Tharp's Thoughts Weekly Newsletter (View On-Line)

-

Article Monthly Market Update by Frank Eaves

-

-

$700 Discount Ends Next Week on April Workshops

Two of Dr. Tharp's Foundation Workshops coming this month, Blueprint for Trading Success and How to Develop a Winning Trading System are almost sold out.

Maximize the value of your time and money by also attending the new Trading in a Bear Market workshop during the same trip to North Carolina. View the newest video from instructor Mark McDowell on shorting a trade.

For our full workshop schedule, including discounts and pricing, click here.

Article

Monthly Market Update, Market Condition: Bull Quiet

by Frank Eaves

View On-line

This month, Frank Eaves has written the Market Update for Van who just returned from a long trip in Asia. Van edited it slightly as he returned.

I always say that people do not trade the markets; they trade their beliefs about the markets. In that same way, I'd like to point out that these updates reflect my beliefs. If my beliefs and your beliefs are not the same, you may not find them useful. I find the market update information useful for my trading, so I do the work each month and am happy to share that information with my readers.

However, if your beliefs are not similar to mine, then this information may not be useful to you. Thus, if you are inclined to do some sort of intellectual exercise to prove one of my beliefs wrong, simply remember that everyone can usually find lots of evidence to support their beliefs and refute others. Just simply know that I admit that these are my beliefs and that your beliefs might be different.

These monthly updates are in the first issue of Tharp's Thoughts each month. This allows us to get the closing month's data. These updates cover 1) the market type (first mentioned in the April 30, 2008 edition of Tharp's Thoughts), 2) the five week status on each of the major US stock market indices, 3) our four star inflation-deflation model plus John Williams' statistics, and 4) tracking the dollar. I will now report on the strongest and weakest areas of the overall market as a separate SQN™ Report. And that may come out twice a month if there are significant market charges.

Part I: Frank's Commentary—The Big Picture

For my big picture process, I try to see if the recent news stories line up with the recent price action in the market. This month the stock market hit new all-time highs. Is the economic news congruent with this price action? Or is there possible divergence between the market price patterns this month and what is going on economically in the world?

The US Economy

This month the jobs report showed the 175,000 jobs were created in February which is higher than the previous two months. The U.S. government’s deficit is 23.6 percent lower than it was at the same time period last year. This indicates the nation's finances may be improving. The Federal Reserve reduced its monthly bond buying by another $10 Billion. A few weeks back, Janet Yellen in so many words said that the Federal Reserve may increase interest rates 6 months after the bond buying program comes to an end. Currently, that would work out to be April 2015. Later in the month, however, she backpedaled her statement a bit with strong language indicating the interest rates would remain low for a long period of time because the economy needed this support. She said she would “Do all that [she] can” to help the U.S. economy where unemployment is too high and inflation is too low.

Speaking of increasing interest rates, New Zealand became the first developed nation to increase interest rates since 2008 because it was concerned about inflation. Stanley Fischer, the nominee to be Federal Reserve vice chairman thinks otherwise as he said the world’s largest economy still needs the central bank’s unprecedented accommodation as joblessness remains elevated. I’m not sure this kind of talk helps the confidence of the foreign nations holding U.S. debt - foreigners sold a record amount of US debt this month.

The U.S. growth for the end of 2013 was revised down by the commerce department from an initial estimate of 3.2 percent to 2.4 percent, an adjustment of 25%.

Equities And The US Consumer

The U.S. stock market may be reaching new highs because of the Federal Reserve’s bond buying, says Dallas Fed President Richard Fisher. Meanwhile, company insiders across the board have been selling their shares at a rate that hasn’t been seen in almost 25 years. That means that you would have to go back further than 2007 and 2001 to find insiders selling more shares.

An affordability study was done that found the average households across the nation can’t afford a new car. On the inflation front milk prices reached a record high this month as more and more milk is in demand and being exported out of the U.S. Not to be outdone, beef prices also posted the biggest price surge in a decade according to the Wall Street Journal.

The Banking Sector

Across the world, the banking sector is getting hit with some really bad news. After being bailed out in 2008 more and more revelations have come to light this month about how those bailouts were truly arranged. George Soros thinks that the banking sector is a “parasite” holding back economic recovery across the globe. Specifically he mentioned the banks “incestuous” relationship with government regulators and believes that little has been done to resolve the core issues that caused the 2008 crisis. Speaking of the GFC, the Wall Street Journal reported this month that banks are now back to issuing adjustable rate mortgages ARM’s for the first time since 2008.

China Concerns and Gold

The Chinese Yuan lost a lot of value against the dollar and there are now fresh concerns over carry trades being forced to unwind because of the leverage involved with carry trades. The New York Times reported that hundreds of Chinese in rural China are doing a run on the banks because of concerns over solvency. China's Chaori Solar became China’s first onshore bond default. China’s CSI index plunged to a five-year low and some claim that it might have been because of an export slump. Trading was suspended for China’s Baoding Tianwei electric company as losses mount. This is again related to bonds that were paying savers a higher interest rate than the banking system is giving. Many current stories concern China’s shadow bank system crashing and what that would mean for the companies and for the Chinese citizens who have money with them. China is also fighting a bursting housing bubble and this is taking its toll on Chinese citizens as well.

Gold was certainly a big player in the news last month. India lightened up on its gold restrictions taking in 38 tonnes of gold in January after buying 25 tonnes in December. Will India take back the title of the largest gold importer in the world from China this year? The ETF GLD took in more than 10 tonnes of gold for the month of February. Gold production in Australia hit a ten year high. There were mixed reports claiming that China’s gold demand is up 51%, 30%, or 29% this year as compared with the same time period from a year ago. Determining how much gold goes into China can be very difficult because of inaccurate reporting and its lack of transparency. We can have some confidence in the following report - China saw the biggest increase in volume of gold future trading on the Shanghai Futures Exchange in the last five years. The exchange also opened up trading futures to foreigners this month. Taiwan has now allowed its banks to sell gold and silver coins made in China. Iraq made the news this month when it was reported that it had purchased 36 tonnes of gold.

Debt in Europe and Beyond

There’s news out of Europe that Italy and France were put on the European Commission's economic "watch-list" over fears about persistently high debt and deficit levels. The IMF has warned of the risks of low inflation and called on the European Central Bank to do more to strengthen Europe’s economy. Also, a leading German institute called for quantitative easing by the European Central Bank to avert a deflationary spiral. Greece still feels the effects of Europe's attempt to fix the banking crisis. The bailout funds have done little to ease the pain which that everyday Greeks continue to suffer. Not wanting to suffer any more austerity measures either, protests in Spain turned violent this month as protesters clashed with police. The European Bank is also considering negative interest rates as another policy tool to stimulate growth in Europe.

The Bank of England seems to agree with Ms. Yellen as it extends stimulus for a sixth year holding its interest rate at 0.5 percent. Ireland was reported to have suffered a big economic slowdown at the end of 2013 which caused a negative growth rate for 2013. In Japan the misery index hit a 33-year high on Abenomics. Japan will increase taxes while prices rise even though wage increases have been stagnant. The economy is apparently equally bleak in Iran as the New York Times reported that new political leader is finding it very difficult to increase economic activity after taking office.

Brazil’s debt was downgraded this month by the S&P to near junk. This can’t be good for the largest economy in South America.

On the American home front at a slightly lower scale, Moody’s downgraded Chicago’s credit rating. The only major city that has a lower rating is Detroit.

Global debt was reported this month to cross a $100 trillion, raised by $30 trillion since 2007. That’s a lot of debt and some are saying that we are heading for a bust like none ever seen.

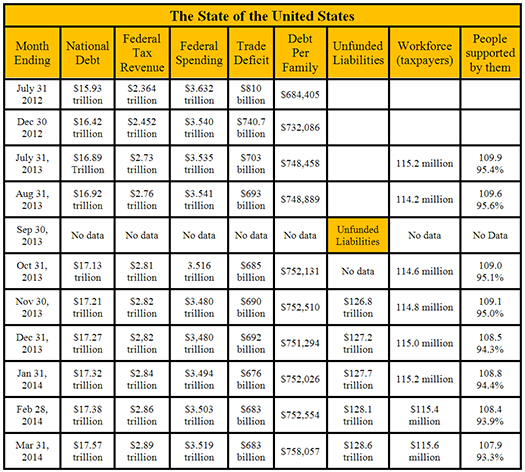

Debt Clock

Right now, total unfunded US liabilities stand at $128.6 trillion with most of that ($89T) being Medicare and ($22T) prescription drug liability. Social security unfunded liability is only a little less than our total debt at $16.9 trillion.

The official US debt is over $17.57 trillion and it’s now going up almost a trillion dollars every year. The debt situation is so bad that the Federal Reserve has driven short term interest rates to almost zero and long term rates to very low numbers. This has killed the U.S. dollar and interest rates have nowhere to go but up. In fact, betting on eventual higher interest rates is about as close to a certain bet (long term) as you could ever make.

According to the debt clock, our official national debt stands at $17.57 trillion, up $19 billion from the prior month. The US population is at 317.8 million with taxpayers standing at 115.6 million. The Boomer retirement wave is in its earliest stages still and retirees now stand at 47.3 million. Disabled people collecting social security stands at 14.3 million while food stamp recipients total 46.3 million so that’s 108 million people that are supported by the government (or the 115.6 million taxpayers). But really about 11.5 million taxpayers pay 90% of U.S. taxes. This means that 11.5 million workers are supporting 108 million other people through the government. Do these numbers add up to you? Do they seem sustainable?

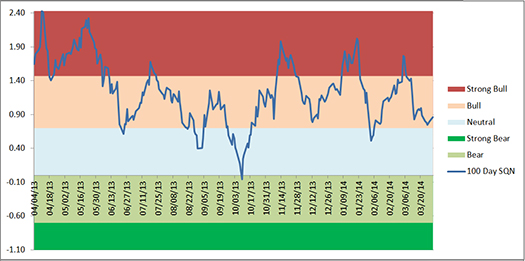

Part II: The Current Stock Market Type Is Bull Quiet

Each month, Van looks at the market SQN® score for the daily percent changes in the S&P 500 Index over 200, 100, 50 and 25 days. For our purposes, the S&P 500 Index defines the market.

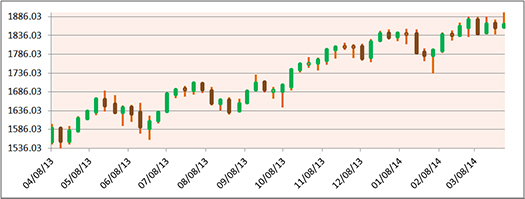

On March 31, the market type for the 200 day period and the 100 day period were both in Bull mode. Van uses the 100 day period to define the market type. For reference, the 50 day and 25 day periods were both in Neutral territory. The following chart has the Market SQN score using the 100 day period and the following chart shows a price chart for the S&P 500 —

(to see the three following charts stacked and aligned, click here)

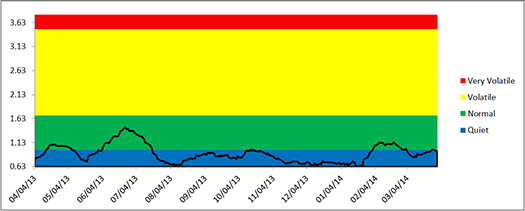

Market volatility is at the edge of normal and quiet range so there may be an element of increasing risk in the market this month compared to last.

(to see the three previous charts stacked and aligned, click here)

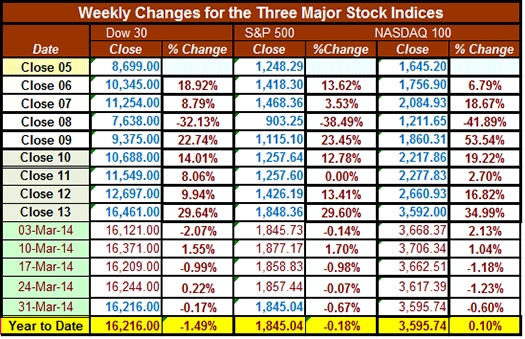

Below is a chart of the weekly changes in the three major US Indices. Two are essentially where they started the year and the third is fractionally down on the year.

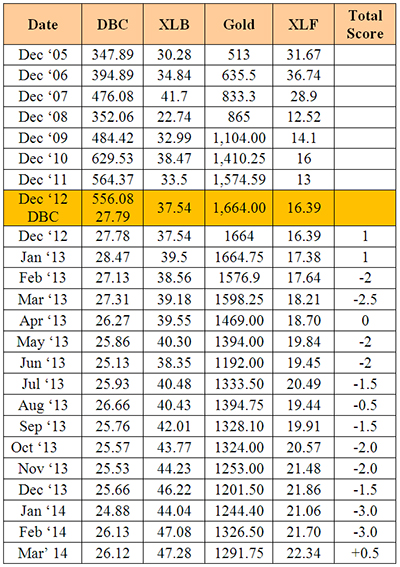

Part III: Our Four Star Inflation-Deflation Model

In the simplest terms, inflation means that stuff gets more expensive, and deflation means that stuff gets cheaper. There’s a correlation between the inflation rate and market levels, so the inflation rate can help traders understand big-picture processes. Here’s the monthly data for each component of the model -

Looking back over the most recent two-month and six-month periods provides the current month’s score, given in the table below.

Month |

DBC2 |

DBC6 |

XLB2 |

XLB6 |

Gold2 |

Gold6 |

XLF2 |

XLF6 |

Total Score |

|

Higher |

Higher |

Higher |

Higher |

Higher |

Lower |

Higher |

Higher |

|

Feb 14 |

|

+1 |

|

+1 |

|

-1/2 |

|

-1 |

+0.5 |

For the first time in 13 months, we see an indication of inflation, although it’s weak. Deflation has been predominant in the last year. As we continually point out, one of the largest deflationary forces comes from banks not lending. The money multiplier put out by the Fed is still at 0.7 rather than the normal 3.0 that we tended to see over recent decades. It’s interesting because the St. Louis Fed discontinued the old data series and now displays the data on a seasonally adjusted basis, however, the graph still clearly says the banks aren’t lending.

Part IV: Tracking the Dollar

Since its peak in July, the USD has been on a downtrend since last July that recently gathered strength into mid March when it broke through the 80 level again. It rose for the rest of the month and finished March at 80.24. In the first few days of April, however, the dollar has again been below 80 which could signal danger for the US stock market. Here’s a chart of daily bars for the index since last June -

General Comments

So the stock market hit new highs in March with no real economic news from around the world supporting new highs. Is the market forecasting large economic growth six months from now? Well six months ago the market was hitting new highs as well yet I don’t see the economic metrics showing strong economic growth.

I have a belief that the market has been going up because of the money being created by the Federal Reserve. The Federal Reserve has indicated this month that it will continue its tapering action and will be cutting another 10 billion from its monthly bond purchases. This may be an indication that the market will now have to support its current lofty levels based on real economic growth - which doesn’t seem to be there. That said, the market type is Bull Quiet and being long in this market isn’t wrong. Based on the economic news that I read, however, keeping a close watch on your stops would be prudent in this market where news doesn’t match the price.

We have a bear market workshop soon and being prepared for what’s inevitable would be sound advice for most of you.

About the Author: Frank Eaves is one of the research assistants for the Van Tharp Institute and has been with the company for about two years. He is a key contributor to software development initiatives and has a current focus on our newest trading simulator. He prides himself in keeping the rest of the office on its toes with his frank and sarcastic sense of humor.

Workshops

Combo Discounts available for all back-to-back workshops!

See our workshop page for details.

Trading Tip

March, 2014 SQN® Report

by Van K. Tharp, Ph.D.

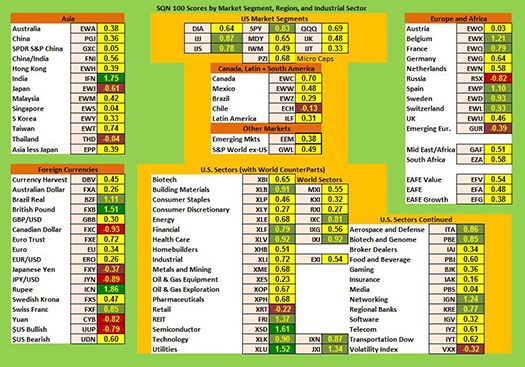

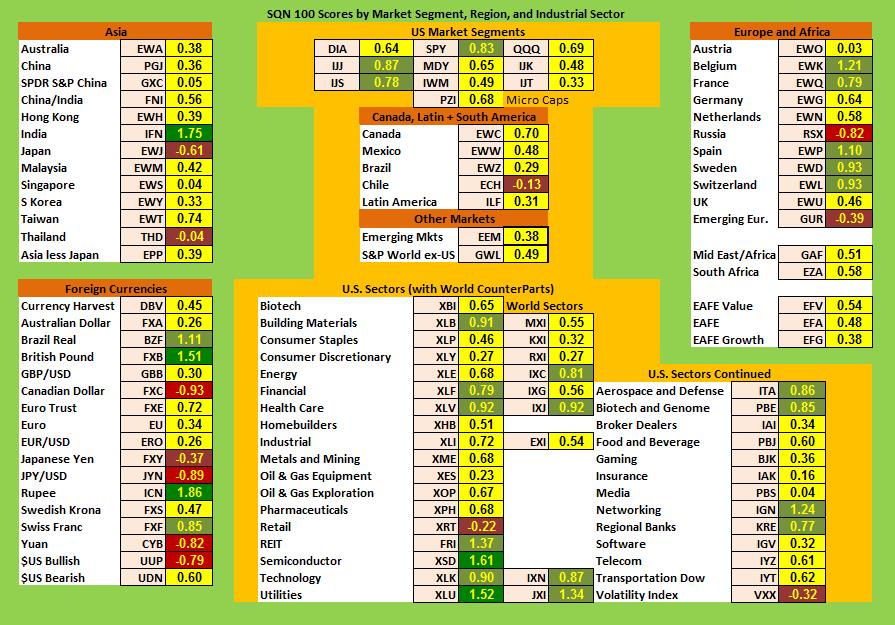

There are numerous ETFs that now track everything from countries, commodities, currencies and stock market indices to individual market sectors. ETFs provide a wonderfully easy way to discover what’s happening in the world markets. Consequently, I now apply a version of my System Quality Number® (SQN®) score to measure the relative performance of numerous markets in a world model.

The Market SQN score uses the daily percent change for input over a 100-day period. Typically, a Market SQN score over 1.45 is strongly bullish and a score below -0.7 is very weak. The following color codes help communicate the strengths and weaknesses of the ETFs in this report:

- Green: ETFs with very strong Market SQN scores (0.75 to 1.5).

- Yellow: ETFs with slightly positive Market SQN scores (0 to 0.75).

- Brown: ETFs with slightly negative Market SQN scores (0 to -0.7).

- Red: Very weak ETFs that earn negative Market SQN scores (< -0.7).

The world market model spreadsheet report below contains most currently available ETFs; including inverse funds, but excluding leveraged funds. In short, it covers the geographic world, the major asset classes, the equity market segments, the industrial sectors and the major currencies.

World Market Summary

Each month, we look at the equities markets by segment, region and sector. Everything has changed since the February report. At the end of February, all US market segments were green and had scores ranging from 1.1 to 1.8 but now they are either light green or yellow with the highest score less than .9 . Europe is still mostly green, but now there is some yellow and Russia and Emerging Europe have turned from yellow to brown/red. In Asia, Japan and Thailand are weak with most sectors being yellow. India, on the other hand, is very strong. And in the Americas (other than the US) everything is yellow (improving) except for Chile which remains negative.

(Click here to see a larger version of this chart)

Most currencies are yellow. The four weakest currencies are the Yen, the Canadian Dollar, Yuan, and US Dollar. The Brazilian Real and Swiss Franc have moved to light green. The Indian Rupee and the British Pound and the strongest currencies.

From a sector standpoint, we are mostly yellow with some green. Utilities and semiconductors are the only dark green sectors. Software, Building, Financials, Biotech, Healthcare, REITs, technology, aerospace, networking and regional banks are light green. Retail and volatility are the only brown sectors and none are red.

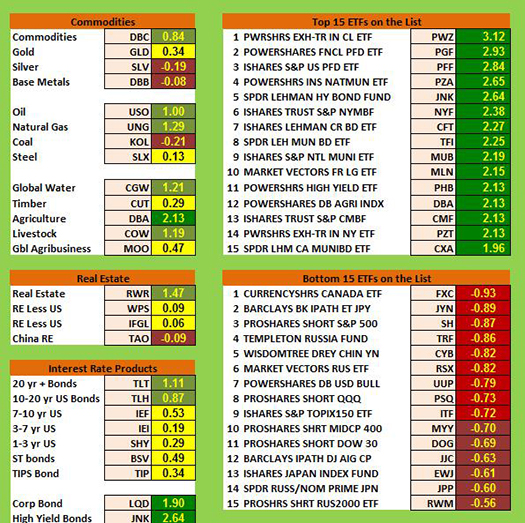

Commodities, Real Estate, Debt, Top and Bottom Lists

The next chart shows the Market SQN scores for the last 100 days in real estate, debt instruments, commodities along with the top and bottom ETFs.

Agriculture is the only dark green commodity. Natural gas, commodities, oil, global water, and livestock are all light green. Metals, however, are still pretty weak but gold has moved up into yellow territory. US real estate is now strong, but Chinese real estate is negative. All the interest rate sectors are positive with Junk Bonds actually being dark green with a SQN score above 2.0 and corporate bonds also being strong. Interestingly, long-term Treasury bonds are now stronger than short term Treasury bonds. Either a lot of people don’t seem to understand what’s going on in the world or they are making short term plays.

In the top market SQN scoring ETFs, we have 14 groups with SQN scores above 2.0 and one above 3.0 which is very rare. PWZ has a score of 3.12 — California Municipal Bonds. Muni-bonds seem to be kings of the heap but preferred stock (PFF) is also up there.

None of the weakest ETFs are below -1.0 and the list includes some currencies and short funds.

Summary

Now let’s look at our newest table which measures the percentage of ETFs in each of the strength categories. Based on this, we are seeing a downward trend. Strong bull moved from 18.9% to 4.9%, and bull moved from 48.4% to 40.2%. The bearish side moved from 13% to 16.4%, but last month was very low.

Date |

Very Bullish |

Bullish |

Neutral |

Bearish |

Very Bearish |

|

> 1.5 |

0.75 - 1.5 |

0 - 0.75 |

0 - -0.7 |

< - 0.7 |

January 31st |

27.1% |

39.6% |

20.7% |

6.4% |

4.7% |

February 28th |

10.3% |

45.2% |

24.4% |

11.9% |

7.5% |

March 31st |

39.2% |

25.5% |

19.1% |

9.0% |

6.4% |

April 30th |

49.1% |

21.1% |

14.8% |

8.0% |

6.2% |

May 31st |

29,2% |

23.6% |

19.9% |

12.3% |

14.2% |

June 30th |

2.1% |

31.0% |

23.2% |

22.0% |

20.9% |

July 31st |

8.2% |

33.5% |

29.0% |

13.3% |

15.2% |

August 30th |

1% |

15% |

46.4% |

19.3% |

17.5% |

Sept. 30th |

1% |

13.8% |

42.3% |

23.0% |

19.1% |

Nov. 1st |

13.3% |

48.3% |

21.8% |

12.5% |

3.3% |

Dec 1st |

14.6% |

42.7% |

24.2% |

13.3% |

4.3% |

Dec 31st |

19.3.% |

45.5% |

22.0% |

11.3% |

2.9% |

January 31st |

8.0% |

49.3% |

20.7% |

12.7% |

7.6% |

February 28th |

18.9% |

48.4% |

18.1% |

6.2% |

6.8% |

March 31st |

4.9% |

40.2% |

38.8% |

13.3% |

3.1% |

What's Going On?

I guess the market likes Janet Yellen — at least for now. The fundamentals are still terrible but the stock market seems like one of the key places to be. However, a bear market could be right around the corner. Be careful.

Until early May, this is Van Tharp.

The markets always offer opportunities, but to capture those opportunities, you MUST know what you are doing. If you want to trade these markets, you need to approach them as a trader, not a long-term investor. We’d like to help you learn how to trade professionally because trying to navigate the markets without an education is hazardous to your wealth.

All the beliefs given in this update are my own. Though I find them useful, you may not. You can only trade your own beliefs about the markets.

About the Author: Trading coach and author Van K. Tharp, Ph.D. is widely recognized for his best-selling books and outstanding Peak Performance Home Study Program—a highly regarded classic that is suitable for all levels of traders and investors. You can learn more about Van Tharp at www.vantharp.com. His newest book, Trading Beyond The Matrix, is available now at matrix.vantharp.com.

Enter the Matrix Contest for a chance to win a free workshop!

We want to hear about the one most profound insight that you got from reading Van's new book, Trading Beyond the Matrix, and how it has impacted your life. If you would like to enter, send an email to [email protected].

If you haven't purchased Trading Beyond the Matrix yet, click here.

For more information about the contest, click here.

Ask Van...

Everything we do here at the Van Tharp Institute is focused on helping you improve as a trader and investor. Consequently, we love to get your feedback, both positive and negative!

Click here to take our quick, 6-question survey.

Also, send comments or ask Van a question by clicking here.

Back to Top

Contact Us

Email us at [email protected]

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

To change your e-mail Address, e-mail us at [email protected].

To stop your subscription, click on the "unsubscribe" link at the bottom left-hand corner of this email.

How are we doing? Give us your feedback! Click here to take our quick survey.

800-385-4486 * 919-466-0043 * Fax 919-466-0408

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute

Be sure to check us out on Facebook and Twitter!

Back to Top |

{kind=link}