Tharp's Thoughts Weekly Newsletter (View On-Line)

-

Article A Trader's Approach to Real Estate Investing: Part Two by Jim Weigel

-

-

-

Seats Now Available in all Three Peak Performance Courses in October

Due to cancellations, we now have a few seats available in both Peak Performance 101 and Peak Performance 203 in October. To register for either, please see our website. Due to cancellations, we now have a few seats available in both Peak Performance 101 and Peak Performance 203 in October. To register for either, please see our website.

We also have one seat available in Peak Performance 202. If you are interested in attending, please call our office at 919-466-0043 for more information or to register.

These are hands-on workshops filled with valuable information that will change the way you look at trading.

The $700 early enrollment discounts for all three workshops expire next week. For more information or to see the full workshop schedule, click here.

A Trader's Approach to Residential Real Estate Investing: A Trader's Approach to Residential Real Estate Investing:

Part Two

by Jim Weigel

View On-line

In part two of this series we are going to discuss real estate market conditions, several real estate investing methods, including the method I’ve used successfully for years, and how you might find similar opportunities. If you missed Part One, click here.

Real Estate Market Types

Market conditions in real estate are noticeably and tremendously important, yet they are rarely used with discipline, even by institutions and “professionals.”

They are noticeable because we see them every day and the data is generally very easy to find on the Internet. While there are a few different kinds of data that are useful, you could determine the market type easily by using permit data, since it is the most useful and the most prevalent.

Here is a simple set of rules, partly implied by Will Rogers, when it comes to real estate market conditions:

- If single family housing permits are going up, then buy, borrow or lend.

- If family housing permits are going down, then don’t buy, don’t borrow, and don’t lend.

- If people want to buy from you, you hit a predetermined target, or permits go down, then sell.

Typical Method for Real Estate Investing

The easiest and most liquid way to invest in real estate is through public securities such as REITs, ETFs, homebuilder stocks and shares of related companies like banks, other mortgage lenders and construction suppliers.

The next most common method is buying homes, whether to fix and flip or to rent and potentially sell. We could include here—buying tax certificates, foreclosures or other distressed properties. While some people invest through partnerships, most operate with the mindset of a self-employed person. Lots of “gurus” market programs that teach these kinds of strategies.

A newer twist on this method is buying properties with all equity and no leverage. Companies (or funds) that practice this method tend to have the mindset of a business owner, with those who finance the method having an investor mindset. The investor must make sure, however, that the operation is run with a business owner mindset and performance discipline, rather than finding out the group just has a nice marketing pitch. I don’t know if any of these funds are really using market conditions to drive their strategies in a disciplined way,1 so you'll need to find that out for yourself if you are interested in these investments.

These days, there is a lot of competition for residential property investments because there are so many individuals and funds chasing them.

My Preferred Method

At the risk of creating a lot more competition for my own method, let me talk about what I do.

Find private homebuilders you like, preferably locally. Lend them money for models, spec homes, pre-sold homes and finished lots; set whatever limits are comfortable for you. Sometimes the investment structure is an equity position rather than a loan. If you have an equity position, you have the option to borrow funds and leverage that position.2

Let’s review two potential deals, a construction loan on a spec3 home and an equity position on a model home.

Spec Construction Loan

Assume a new home will have a $300,000 value, 80% construction and finished lot costs, and that you are financing 100% of those costs, or $240,000. Say it takes four months to build and sell the home. On average, you tend to have 60% of your funds advanced, with 90%-100% advanced by the time it is sold and you get your money back.

Let’s say you charge a 1% fee, a 6% annual interest rate, and 10% of the sales price over $240,000 as a “kicker.” What is your return? You get 6% annual interest rate, but the annualized effect of the fee and the kicker really improve the return. The fee provides 3 1/3% (1%/60% x 12/6) and the kicker provides another 3% [($300,000 - $240,000) x 10%/60% x 12/6]. The total annualized return, then, is 12 1/3%.

Not bad for 3-6 month money, eh?

Model Home

Using the same figures, let’s say this home will be a sales model. In this case, the builder wants to improve his balance sheet and you want a good return over a longer time. For this type of situation, we might want to modify the structure a bit.

First, set up a limited liability company. Your LLC buys the finished lot from the builder for $60,000 and gets a construction/permanent loan from a bank for $180,000. The builder agrees to build the house, furnish it, and rent it from your LLC, then sell it and split the profits 50/50. The bank lends at 2% fees and costs, 7% annual interest rate, interest only payments for 5 years. The builder rents it for $2,500 per month once it is complete and sells it three years later for $330,000.

In this case, you have invested $63,6004, and have personally guaranteed a $180,000 loan, which includes an interest reserve for six months. You get $30,000 rent per year for 2 ½ years ($17,400 after interest) and 50% of the profit when it is sold. Assuming 5% selling expenses, there is $73,500 of profit and your share is $36,750. This yields about 10.1% annual return on your funds. Compared with the yield on three-year bonds, that’s not too shabby, is it?

Deeper Into My Method

While I approach this method with the mindset of an investor, I also integrate the mindset of a business owner - that of one which invests in assets used by homebuilders. There is a financing need and a reasonable risk/reward structure for every asset homebuilders use: land, lots under development, finished lots, pre-sold homes under construction, spec homes, model homes, furnishings, equipment and vehicles. There is even a way to finance software.

Not only must you understand and choose the structure, return and repayment requirements for yourself, you must understand the same elements of the deal from the homebuilder's perspective and help them see how these affect their business. For example, you’ll need to think through -

- How much of your investment should be in the form of a loan versus preferred equity versus common equity.

- What is a reasonable return? (for now, that seems to be about 8%-18% per annum)

- How much time do you want to be invested in an asset? (usually this ranges from three months to three years)

- How much leverage will you choose to employ?

- How much personal recourse should you provide to those who lend to you, and how much should you require from those to whom you lend?

- How much communication will you need with the builder and in what form?

- How will you monitor your investment, your builder, and the market?

Next, you must understand contingencies, plan for them and commit to executing on those plans when the time comes. Encourage or require this of your deal structure and builder as much as possible also. The examples above all assume normal conditions but what happens if things go a little worse than expected? A lot worse? How about the absolute worst case scenario? What will the builder do? What will you do? How do you define “worse” and “worst”? On the other hand, what if things go really, really well?

Then, you must develop your position sizing plan. How much of your total assets will you invest in this “system”? How much will you place with any one builder? In any one deal? How will that change if market conditions worsen? Improve? How will you monitor those market conditions?

Probably the most significant aspect of real estate investing is your commitment and discipline to your position sizing strategy when market conditions falter. For example, if permits in an area drop for four months in a row or have dropped in six of the last nine months, I don’t invest in any new deals. Following these rules, however, causes me to miss deals and it has even caused me to lose relationships because I won’t consistently invest in new deals. When conditions worsen, what will you and your builder do with existing deals? Consider that beforehand rather than at the onset or in the middle of the next decline.

Finding Nemo

Obviously, you want relationships with good businesspeople who build good products in good places. You’re going to have to learn to define what “good” means, and what the signs of “bad” are. Here are the kind of builders I have found make good candidates for my investing:

- Look for local families who have built near you for years. While they may not need an investment from you, they can see that they take on lower risk with your funding. Many of these families have a “self-employed” mindset so you might get a lower return, but it will probably be a more stable investment.

- There are a few builders around who have had the “business owner’ mindset for a while, including some of the families I mentioned above. Business owner builders are distinguished by strong processes in land, design, sales and production. Also, they tend to have regular, simple and meaningful management reporting.

These are the types of homebuilders I want to work with, no matter where they are located because they will provide the best returns and lowest risks. Overall, low-key people in construction who run a good operation are the kind of people with whom I like to associate.

Opportunities and people in real estate are all around us ready for buying, selling, renting, lending, managing, and building. Perhaps some of those people and opportunities fit you.

End Notes

1. Just because I don’t know of any doesn’t mean there aren’t some. I don’t follow this industry or “space” much.

2. You can leverage loans you make, too, but that is more complex and requires a relationship with a bank that is comfortable with that business.

3. A spec home is one that is started without having a sale contract in place with a homebuyer.

4. Includes $3,600 for loan fees & costs.

About the Author: Jim Weigel has had a career in real estate finance, development and construction. In addition to trading, he currently consults with companies in the construction industry. He lives with his family in the Denver, CO area.

Back to Top

Trading Education

We are excited to release our November schedule which includes two brand new workshops, presented by Ken Long.

October 3-5 |

Peak Performance 101

with Van Tharp

Limited space still available. |

| October 7-10 |

Peak Performance 202

Only one seat available, please call 919-466-0043 to register. |

| October 12-14 |

Peak Performance 203

with Van Tharp

Due to cancellations, a few seats have opened. |

| November 8-10 |

Swing Trading Systems Workshop

with Ken Long

8:00am-4:30pm |

| November 8-10 |

NEW! Turbo Charge these Swing Systems

with Ken Long

6:00pm-9:00pm

Stay late and Ken will show you how to use swing trading systems to catch intra-day moves. |

| November 11-12 |

NEW! Live Trading for Turbo Systems

with Ken Long

2 days of live trading alongside Ken Long |

November 16-17 |

Oneness Awakening Weekend

with Van Tharp and Janie Guill |

December 8-15 |

The Annual Super Trader Summit

Click here to learn about the Super Trader Program |

To see the full schedule, including dates, prices, combo discounts and location, click here.

2014 dates will be coming in the next few months. If you are in South Africa and would like have Van host a workshop there, please contact us at [email protected]. There is a possibility he will be visiting South Africa in early to mid 2014.

|

Back to Top

Trading Tip

Five Years Later — Five Years Later —

The Impact of the Real Estate & Credit Collapse

by D. R. Barton, Jr.

View On-line

In a society that is constantly hungry for news, the media happily provides it in all shapes and colors. This week, we will get plenty of reports on the five-year anniversary of the Lehman bankruptcy, which was the trigger for the largest drop in the 2008 financial market meltdown.

As usual, a lot of the reporting has been pabulum. But alas, I have stumbled upon a few resources that are quite insightful, including a cool graphic from The Economist and a staff research paper out of the Dallas Fed entitled “How Bad Was It? The Costs and Consequences of the 2007-2009 Financial Crisis” by Atkinson, et al.

In short, the bubble that burst ate up a significant amount of financial resources, albeit from a bubble-inflated level (no surprise there). But the magnitude of what happened is still surprising. Let’s dig in…

That Much? Really??

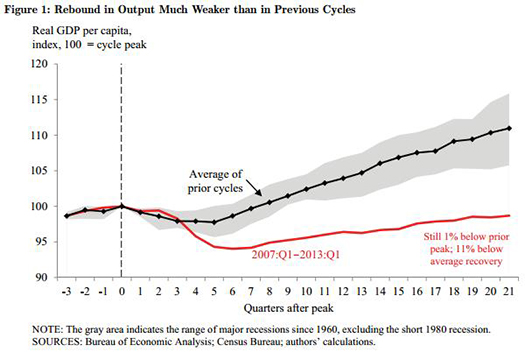

We’ll start with a chart from the Atkinson paper that shows graphically what most people already can intuit from the marketplace around them: this drop and slow recovery have both been much worse than previous cycles.

Of note is that the black line (average) and the grey area (upper and lower extremes) only cover the recessions since 1960 (i.e. no Great Depression data). But it is striking that GDP has not recovered to pre-crisis levels, even more than 5 years later.

In addition, Mr. Atkinson and company do an in-depth analysis on the actual cost of the crisis. They break the effect into several components, starting with lost U.S. output. The authors estimate that between 6 and 14 trillion dollars, or 40%-90% of 2007 GDP was lost.

The research paper lists a large number of other less calculable costs including:

- Unquantifiable cost of national trauma

- Unintended consequences of government intervention

- Cost of reduced wealth

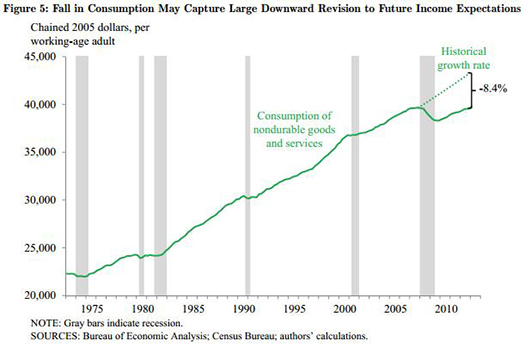

The authors provide a very interesting (and alarming) chart showing the effect of reduced wealth on the purchase of nondurable goods.

This reduced consumption could be linked to both reduced wealth and cutting back spending habits due to reduced future income expectations. But for whatever reason, this reduction in consumption is again worse than we’ve experienced as a nation during previous recessions.

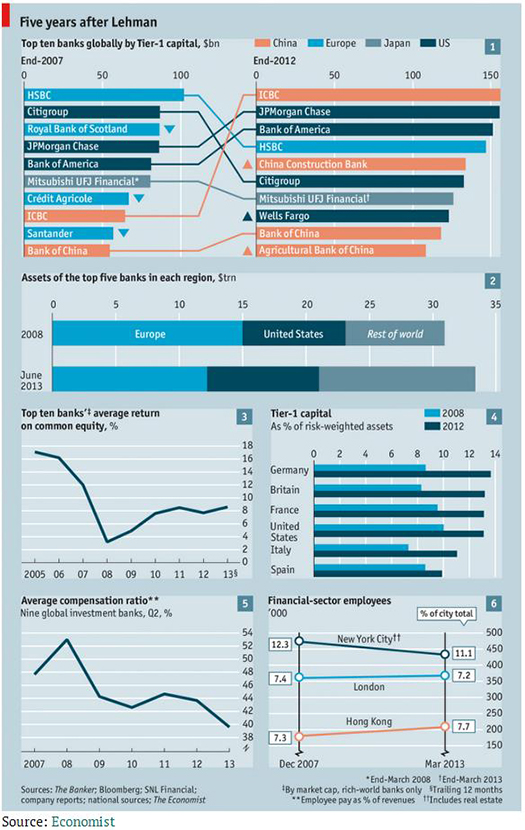

The Economist also weighed in on the after-effects of the crisis with a pretty cool visual, which gives six distinct looks at before, during and after the crisis.

Based on our recent series on China’s woes, the changing bank landscape is a bit troubling. In 2007, the top Chinese banks were numbers 8 & 10 (based on Tier 1 capital). Now, China has four of the top 10 including numbers 1 & 5.

The second chart in the visual above gives an interesting perspective on the contraction in the large banks of Europe over the past five years and the growth in non-European, non-U.S. Banks.

Charts 3, 5, & 6 are pretty self-explanatory. Chart four is worth a mention because, by the measure of Tier 1 capital vs. risk-weighted assets, it seems that banks across the board have improved significantly. Whether this is enough to weather the next contraction remains to be seen.

As always, your thoughts and comments are welcome - please send them to drbarton “at” vantharp.com

Great Trading,

D. R.

About the Author: A passion for the systematic approach to the markets and lifelong love of teaching and learning have propelled D.R. Barton, Jr. to the top of the investment and trading arena. He is a regularly featured guest on both Report on Business TV, and WTOP News Radio in Washington, D.C., and has been a guest on Bloomberg Radio. His articles have appeared on SmartMoney.com and Financial Advisor magazine. You may contact D.R. at "drbarton" at "vantharp.com".

Disclaimer

Back to Top

Matrix Insights

Don't forget to submit your insight for the Matrix contest for a chance to win a free workshop! Don't forget to submit your insight for the Matrix contest for a chance to win a free workshop!

We want to hear about the one most profound insight that you got from reading Van's new book, Trading Beyond the Matrix, and how it has impacted your life. If you would like to enter, send an email with your insight to [email protected]. If we publish your insight you'll also get a $20 VTI gift certificate for VTI products.

If you haven't purchased Trading Beyond the Matrix yet, click here.

For more information about the contest, click here.

For Absolute Beginners

If you are new to trading and want to learn the basics of trading the Tharp Think way, our ABCs of Trading E-learning course is right for you.

- Do you want to figure out what markets and what types of trading might suit you?

- Are you at a loss for how to begin?

This course will answer those questions (and many more) in easy-to-follow lessons written in terms that any trading novice can understand.

Only $49.00

Click here to learn more.

Ask Van...

Everything we do here at the Van Tharp Institute is focused on helping you improve as a trader and investor. Consequently, we love to get your feedback, both positive and negative!

Click here to take our quick, 6-question survey.

Also, send comments or ask Van a question by clicking here.

Back to Top

Contact Us

Email us at [email protected]

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

To change your e-mail Address, e-mail us at [email protected].

To stop your subscription, click on the "unsubscribe" link at the bottom left-hand corner of this email.

How are we doing? Give us your feedback! Click here to take our quick survey.

800-385-4486 * 919-466-0043 * Fax 919-466-0408

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute

Be sure to check us out on Facebook and Twitter!

Back to Top |