Tharp's Thoughts Weekly Newsletter (View On-Line)

-

Article The Superiority of SE Bands by Ali Moin-Afshari

-

-

Trading Tip Why Unemployment Numbers Matter by D.R. Barton, Jr.

-

Ken Long's Day Trading and Live Day Trading Workshops Ken Long's Day Trading and Live Day Trading Workshops

This August, Ken Long will be presenting his popular Day Trading Systems workshop, along with its hands-on counterpart, Live Day Trading. By attending these two workshops, you will have the opportunity to master Ken's Frog and RLCO systems and then trade them live, under the guidance of your instructor.

Click here for more information about these and other workshops.

Why Band Trading Works Why Band Trading Works

Part 3 - The Superiority of SE Bands

by Ali Moin-Afshari

View On-line

In the previous two parts of this series, we analyzed price trends and looked at how some popular bands are built and used. In part 3 of this series, we will look at Standard Error Bands and why I consider them to be superior bands. In favor of saving time and space, I will not get into many of the mathematical details.

Using Statistics to Build Trading Bands

One of the best ways to build trading tools is to use advanced statistical techniques to analyze price action. Typically, bands are built around a central trend line. Therefore, statistical methods that measure trends can be used to define the core bands component — the trend line. Regression analysis is a statistical method with several different applications, among them is trend identification. SE Bands are built on the concept of linear regression.

Price data has three components: long-term or secular trend, short-term trends or cycles, and time. Regression analysis uses statistical measurements to identify the main component of a time series — the trend. Regression analysis can identify price direction over a specific time period without being influenced by cyclic patterns or short-term trend. The part of data that cannot be explained by these three elements is considered random or unaccountable price action.

Selection of a calculation period is important in regression analysis. Different calculation lengths can be used to isolate shorter-term trend within longer term ones, which otherwise would be classified as random. Since short-term trends lead to long-term trends and the end of an old trend is preceded by changes to short-term price behavior, regression analysis provides an effective tool for finding and trading trends.

(to see a larger version of this chart, click here)

Figure – 1: One Year Daily Chart of the ES (S&P 500 futures): Do you believe an indication of bull markets is when price is above EMA200? Comparison of different lengths of Linear Regression lines (curves) with Exponential Moving Averages shows linear regression identifies trend sooner and more accurately than moving averages.

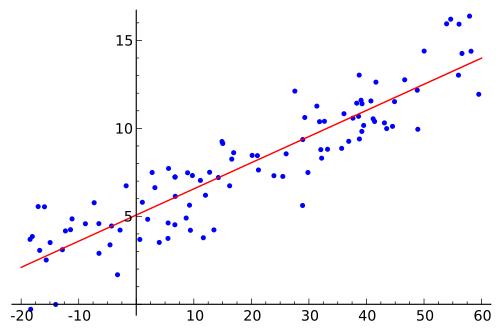

Figure – 2: A Scatterplot and Linear Regression Line:

if each dot considered as the closing price, regression line defines the trend.

Linear regression lines can be thought of as statistically-based trend lines. The mathematical method used to calculate the regression value is called “the least-squares method.” The regression line is drawn straight through the center of the data such that it is the best overall trend line of data points above and below it. This line represents the equilibrium point of the data since half of the data points are above the line and half are below. Extreme values above or below the line tend to retrace towards the regression value.

Standard Error as a Measure of Volatility

Throughout the development and testing of a trading system, we want to know if the results we are seeing are as expected. The answer will always depend on the size of the data sample and the amount of variance in the data during this period.

One descriptive measure called the Standard Error (SE) uses the variance which estimates the error based on the distribution of the data using multiple data samples. It is a test that determines how the sample means differ from the actual mean of all the data. It addresses the uniformity of the data.

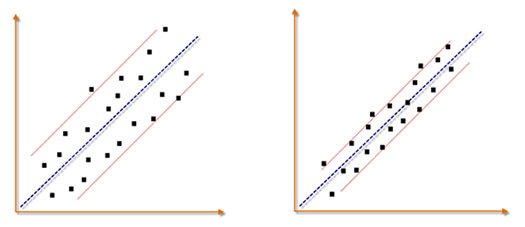

Figure – 3: Standard Error as a Measure of Volatility around a Regression Line:

The Standard Error is higher in a volatile trend (left) and lower in an efficient trent (right).

Put simply, standard error is an estimate of how close to the population mean (i.e. linear regression line) your sample mean is likely to be (Fig. 3), whereas standard deviation is the degree to which individuals within the sample differ from the sample mean (i.e. average price or moving average line). Standard error should decrease with larger sample sizes, as the estimate of the population mean improves. Standard deviation will be unaffected by sample size.

Standard error can be used as a measure of volatility around a regression line (Figure 4 below). Data points produced from an efficient trend are generally tightly dispersed around a regression line. There are no or very few outliers and the regression line is a good representation for the trend. As volatility expands, closing prices scatter and data points are found at various distances to the regression line, which increase the standard error of variance. Therefore, the accuracy of regression can be estimated by calculating the standard error of variation. In trading, volatility can be measured by calculating the standardized variation around the regression line and used to estimate the accuracy of regression. In other words, standard error tells you how reliable your trend line (i.e. regression line) is at each price bar.

(to see a larger version of this chart, click here)

Figure – 4: Standard Error Bands:

1-Year Daily chart of ES with 21-period SEB at ±2 Standard Errors

SE Bands

The above concepts can be applied to band trading to create a band that can tell us at the close of each bar:

- Is new price action conforming uniformly to past price action?

- Is trending behavior expected to continue?

- How efficient is the trend?

- Is the amount of noise in price action increasing or decreasing?

- Is price action in a sideways channel?

- If price is consolidating, is trending behavior expected to begin?

Standard Error bands were invented by Jon Andersen as a trend following indicator. SE Bands are built around a linear regression line using the standard error of regression. First the linear regression value is calculated. Then a short term simple moving average of it is calculated to smooth it out. Next, the standard error value is calculated and smoothed similarly. Then, the first average is plotted and the second average (SMA of SE) is multiplied by ±2 and plotted up and down. Andersen recommend following values for SE bands:

- Number of periods: 21,

- SMA smoothing: 3 periods, and

- Standard error multiplier: ±2

The interpretation of SE bands is very different from Bollinger Bands:

- Tight bands indicate standard error is low and price is moving orderly in the direction of the prevailing trend. One can expect the current trend to continue.

- When bands are wide or expanding there is a higher chance that current trend might slow down, go sideways, or even reverse. Price is losing its directionality and momentum, which means noise is increasing.

Different look back periods and other SE multipliers produce different results. For example, I like longer SE bands such as the 34-period SEB depicted in figure 5. In this case, one of my trading systems says: Enter after two subsequent closes outside the bands in the direction of the RL, when bands are narrow. If I am in a trade already, stay with the trend.

(to see a larger version of this chart, click here)

Figure – 5: Standard Error Bands:

1-Year Daily chart of ES with 34-period SEB at ±2 Standard Errors

SE bands do not have the lagging problems of Bollinger bands and to some extent Keltner channel, discussed in part 2 of this series. SE bands react more quickly to changes in price action and generate signals much faster than other band techniques. Since SE bands are based on regression analysis, the bands are build around a true mathematical measure of price trend rather than the less accurate average price used by other bands. Figure 1 shows there is a considerable difference between same period EMAs and RLs.

Summary

Regression analysis helps traders analyze trends more accurately and SE bands can help them understand the reliability of the trend. SE bands offer a number of trading system development opportunities once traders understand how they interact with price. In the last article of this series, we will explore ideas for building a trading system based on bands.

“Man has two legs, Money has four. Let Money chase you.”

– Chinese Proverb

About the Author: Ali is an IT architect based in Toronto, Canada. He started trading options in 2006. Despite early success, he realized he needed both a deeper understanding of self and of trading to ensure continued success. Reading Dr. Tharp’s books brought him to Cary to take part in various IITM courses. Ali has spent the past five years studying and perfecting his trading. He is planning to move to full time trading after completing his current technology consulting project.

Trading Education

The Frog day-trading system has multiple intraday opportunities every day the market is open. Positions are closed by the end of the day, so there’s no overnight risk or worrying about positions while you lay in bed at night. The Frog system is part of the Day-Trading Workshop in August.

July 13-14 |

Core Trading Systems

with Ken Long

SOLD OUT

|

| August 10-11 |

Oneness Awakening Weekend

with Van Tharp |

August 16-18 |

Day Trading Systems

with Ken Long

Learn Ken's Frog and RLCO systems

|

August 19-21 |

Live Day Trading

with Ken Long

Day Trading Systems is a prerequisite to this course.

|

October 3-14 |

Peak Performance 101, 202 and 203

Register for Peak 101 and get on the waiting list for 202 and 203 now.

|

| Berlin, Germany Workshops |

September 6-8 |

How to Develop a Winning Trading System

with Van Tharp and RJ Hixson

|

September 10-12 |

Blueprint for Trading Success

with Van Tharp and RJ Hixson

|

September 14-16 |

Forex Trading

with Gabriel Grammatidis

|

Register for all 3 and save $800!

|

To see the full schedule, including dates, prices, combo discounts and location, click here.

Trading Tip

A Deeper Look at Unemployment Numbers: Part 3—

Why Unemployment Numbers Matter

by D. R. Barton, Jr.

View On-line

Since last week’s article, Dr. Bernanke and the good folks over at the Fed have spoken — and spooked the market. They didn’t even have to take the punch bowl away to make the bull party turn sour, all that was needed was the acknowledgement that the sugary goo would, in fact, be taken away at some time in the future…

The number one mover of markets today is each and every utterance from any central banker. Here is what has happened since we spent time together on the last written page (These summer weeks really fly by, don’t they?):

- The Fed’s pronouncements precipitated a 6% drop from Tuesday’s (6/18) close to Monday’s (6/24) lows.

- The People’s Bank of China tightened their monetary policy for Chinese banks and the Shanghai Composite Index dropped 5.2% in one day.

- And just last night (Tuesday), the European markets leapt 2% when European Central Bank chairman Mario Draghi merely said he was “ready to act”! No plan, just “ready to act”…

The bottom line — central bankers’ words and actions are driving the markets. Period.

At this point, it’s necessary to interject here why employment is even minimally important to us as traders and investors Dr. Bernanke & Co. have said that they will keep the easy money spigot open until unemployment drops to 6.5% percent. Especially for these times then, we have to remain attuned to the machinations that are part of the unemployment reporting game.

Employment Numbers Aren’t Telling the Real Story (Surprised?)

Ok, so that heading is a massive understatement. Let’s drive on and look at some facts (and some cool charts) that will provide us with some backup.

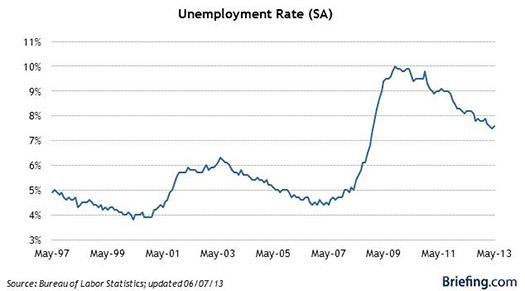

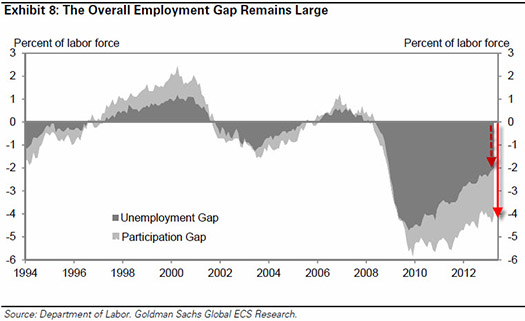

First of all, things aren’t as rosy as they seem in employment land. Sure, the Bureau of Labor Statistics (BLS) number is going down, we’ve looked at the chart before:

There are mitigating circumstances that make this seemingly positive trend seem hollow — so much so that Goldman Sachs issued a much-distributed report that bluntly stated, “The Unemployment Rate is an inappropriate measure of the labor market.” Let’s look at some of the reasoning and some of their charts that found their way to Zero Hedge. The bottom line is that the infamous “labor participation rate” has continued to drop which makes the unemployment numbers look better than they really are. Politically expedient reasons (gasp!) account for the apparently improving unemployment statistic but Goldman suggests (insists?) that the Fed use a number other than the BLS figure to drive monetary policy.

Where Are the Problems with the Employment Numbers?

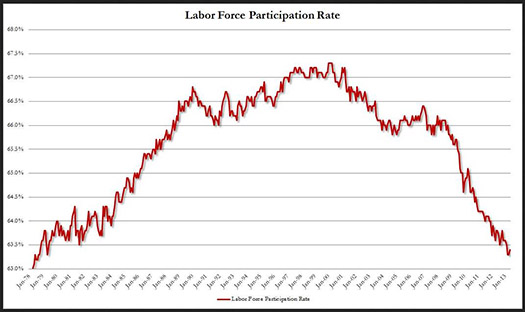

Are more people really finding jobs or are more being classified as inactive? Here’s a chart showing the decline in participation:

First, note that this scale is magnified (the difference between best and worst numbers is only 4.5%). But remember that a 1% change in a population of 311 million ends up being a huge number!

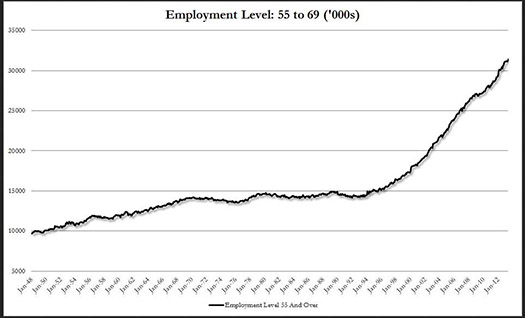

The first reason that people give for this decline in participation is that the U.S. population is aging, and that is taking people out of the workforce. If that’s the case, then how do they explain the chart below?

Does this chart show retirement-aged people are dropping out of the workforce? And while more and more Baby Boomers hit retirement age every year, that number certainly hasn’t doubled since the late 1990’s… (This chart is not from the Goldman Sachs report.)

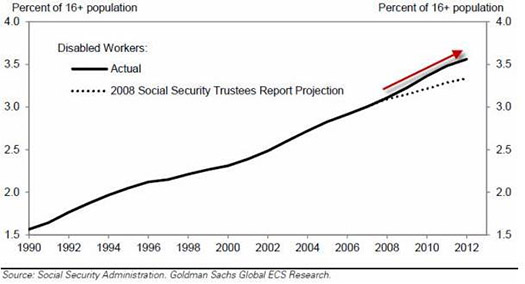

And now for the scariest chart of the day — here is one reason that labor participation has gone down, and it’s a trend that needs to be addressed:

Notice the acceleration in the percentage of the population that is now receiving disability — a number that has has taken a jump since the 2008 financial crisis, and more importantly, has more than doubled since 1990. Since 2007, 1.75 million people have been added to the Social Security Disability Insurance system. That’s almost 0.6% of the total U.S. population!

Let’s not be naïve — we need to remember that Goldman has a dog in this hunt. As long as the Fed keeps the money machine pumping out the lubricant, the bankers continue to have a huge business advantage versus tighter monetary policy periods. The reason is simple — the more money in circulation means more profits for those who get paid for moving it around.

With that said, Goldman did have a well-reasoned conclusion that seems worth repeating in toto

The more immediate implication is that Fed officials may need to revisit their forward guidance. In principle, we see three options for what they might do, in increasing order of aggressiveness:

- Emphasize that 6.5% is only a threshold. They could emphasize even more that the 6.5% figure is only a necessary, but not sufficient, condition for a hike. This is the simplest option because it does not require agreement on a new measure. However, it would make forward guidance a less and less powerful instrument of monetary policy; thereby, it would violate the principles laid out in Michael Woodford’s 2012 Jackson Hole Paper on monetary policy accommodation at the zero bound, which seems to enjoy widespread acceptance among many FOMC members.

- Change the number. They could lower the 6.5% threshold while keeping the focus on the unemployment rate. This would be a pragmatic way of adjusting the current approach for the participation issue without having to introduce new and less widely followed labor market indicators into the FOMC statement.

- Change the measure. They could directly couch their guidance in terms of the employment to population ratio (presumably adjusted for the effects of population aging), our total employment gap shown in Exhibit 8, or a participation gap — adjusted unemployment rate. This directly addresses the underlying issue, namely that the unemployment rate has become a less useful statistic. But it would be considerably more complicated in terms of communication.

Financial markets continue to expect a very late exit, despite the declining unemployment rate, so Fed officials may not feel much urgency in revamping their forward guidance. But as we approach 6.5%, a reduction in the threshold or maybe even a new measure may well be necessary.

Up Next Friday?

Next Friday (July 5th) will mark the next announcement of BLS numbers which could either move the markets or turn out to be a blasé affair. Be aware that an uptick in unemployment could bring on the counter-intuitive result of the equities markets going up. Why? Some could see a negative employment report as delaying the Fed’s inevitable taper of their current monthly dose of market morphine.

As always, your comments and feedback are welcome! Please send your thoughts to drbarton “at” vantharp.com

Great Trading,

D. R.

About the Author: A passion for the systematic approach to the markets and lifelong love of teaching and learning have propelled D.R. Barton, Jr. to the top of the investment and trading arena. He is a regularly featured guest on both Report on Business TV, and WTOP News Radio in Washington, D.C., and has been a guest on Bloomberg Radio. His articles have appeared on SmartMoney.com and Financial Advisor magazine. You may contact D.R. at "drbarton" at "vantharp.com".

Disclaimer

Important Update

Important Update Important Update

by Van K. Tharp, Ph.D.

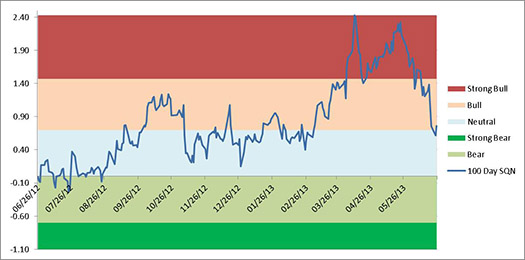

While I won’t write another full market update until next week, it’s important to note that the market type has changed significantly since the last update on June 5th. If you look at the following chart showing the 100-day market SQN® rating, you will see that the trend is clear:

The 100-day market SQN score has moved from strong bull to bull very quickly and is now at the borderline with neutral territory. The trend in the chart says it all and the shorter term market SQN scores confirm that trend. The 50-day market SQN rating is in neutral territory and the 25-day market SQN rating is now STRONG BEAR. In addition, market volatility moved from quiet to normal and its current trend is heading toward more volatility.

This is becoming a dangerous market; it is not a time for “buy and pray” investors. If you are active in the market, you need to know what you are doing or you could be one of those people in a future workshop who might be saying “I wish I had known that back in 2013.”

We have what is probably one of the biggest bubbles in the history of the U.S. financial markets — bond prices. Interest rates have dropped ridiculously low. In fact, they cannot be much lower despite owing the greatest debt in the history of any country in the world. When this bubble bursts, and the Fed is now implying that it might start tapering their current round of QE soon, it will be a disaster for most markets. Not only will bond prices crash, but the stock market will as well. Be prepared to protect yourself.

Most importantly, make sure you are clear. This is a time for neither fear nor greed. For those who are sharp and well trained, this could be a time for tremendous profits.

Ask Van...

Everything we do here at the Van Tharp Institute is focused on helping you improve as a trader and investor. Consequently, we love to get your feedback, both positive and negative!

Click here to take our quick, 6-question survey.

Also, send comments or ask Van a question by clicking here.

Back to Top

Contact Us

Email us at [email protected]

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

To change your e-mail Address, e-mail us at [email protected].

To stop your subscription, click on the "unsubscribe" link at the bottom left-hand corner of this email.

How are we doing? Give us your feedback! Click here to take our quick survey.

800-385-4486 * 919-466-0043 * Fax 919-466-0408

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute

Be sure to check us out on Facebook and Twitter!

Back to Top |